The Philippines just kicked off its first offshore wind auction, and frankly, it's about time. The country sits on a goldmine of wind resources – 178 GW worth – yet has been frustratingly slow to capitalise on this natural advantage until now.

Success or failure hinges on whether developers can secure affordable financing to hit that ambitious 50% renewable target by 2040. The good news? There's already 66 GW under service contracts, proving developers are queuing up for this opportunity.

Getting the Wind Behind Philippine Sails

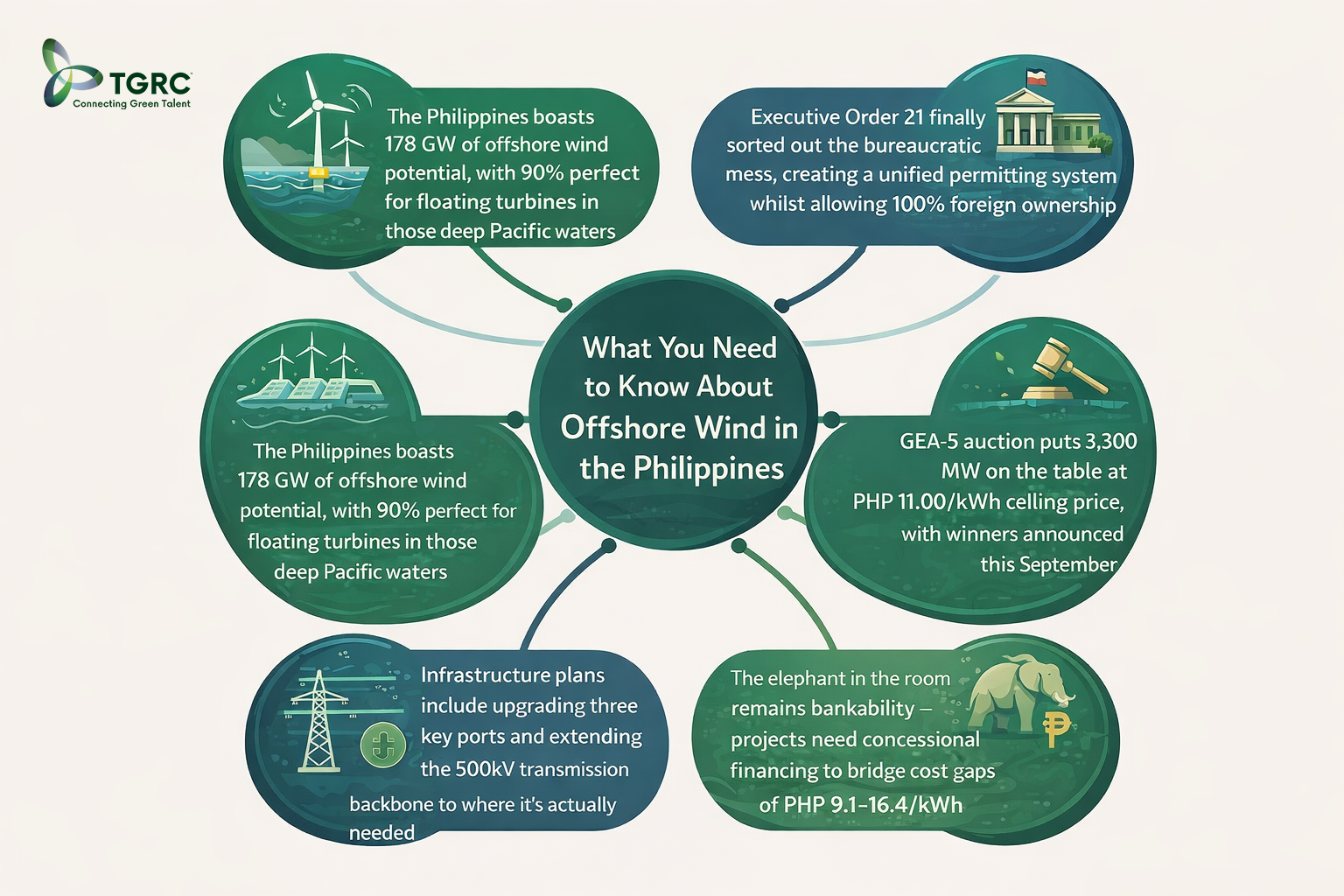

When the Philippine government finally pulled the trigger on its inaugural offshore wind auction last November, it wasn't just another policy announcement. This was the starting gun for a sector that should have been racing ahead years ago, given the archipelago's exceptional wind resources of 178 gigawatts. The target of 50% renewable energy by 2040 suddenly looks achievable rather than aspirational 2.

What makes this particularly interesting is how the World Bank's Offshore Wind Roadmap has provided the technical backbone for these ambitions, whilst regulatory reforms have cleared away the bureaucratic debris that typically strangles good projects in their infancy 4. The combination of South Luzon developments and serious investment from players like Copenhagen Infrastructure Partners suggests this isn't just another government wishlist, but a market with genuine commercial momentum.

Building the Policy Foundation for Offshore Success

National Renewable Energy Programme targets

The National Renewable Energy Programme sets out an ambitious trajectory for the Philippines' energy future, targeting 35% renewable energy share in power generation by 2030 and 50% by 2040 5. These figures aren't just aspirational - they require adding 52.8 GW of new renewable capacity across multiple technologies: 16.7 GW from wind, 27.2 GW from solar, 6.2 GW from hydro, 2.5 GW from geothermal, and 0.4 GW from biomass3. Offshore wind represents a crucial component of that wind capacity expansion, particularly given the archipelago's geography.

Executive Order 21 and regulatory reforms

President Ferdinand R. Marcos Jr. signed Executive Order 21 on 19 April 2023, instructing the Department of Energy to create a unified policy framework for offshore wind development6. The order tackles a genuine problem - fragmented permitting across multiple agencies that had been causing significant project delays3. The DOE followed through quickly, releasing Department Circular DC2023-05-0013 on 18 May 2023, which established clear guidelines for offshore wind development stages and their corresponding permit requirements 7.

What makes this approach notable is its whole-of-government philosophy. Rather than leaving developers to navigate bureaucratic silos, the framework demands coordination across all relevant departments7. Every permitting agency had 60 days to submit their complete requirements, fees, and procedures 6. The DOE now reviews these submissions for integration into the Energy Virtual One-Stop Shop platform, creating a single access point for developers6.

Foreign investment liberalisation

The Department of Energy's Circular 2022-11-0034, issued in November 2022, removed the previous 60% Filipino ownership requirement for renewable energy projects 8. Foreign investors can now hold 100% equity in Philippine entities engaged in solar, wind, hydro, and ocean energy activities3. This reform represents a significant shift from the protectionist policies that had previously limited international participation in the offshore wind market, allowing companies complete operational and profit control 3.

Green Lane certification for faster approvals

Executive Order 18, launched in February 2023, established the Green Lane programme to expedite strategic investment approvals 9. The results speak for themselves - the Board of Investments has certified 232 projects worth PHP 6.11 trillion through 31 December 2025, projected to create 398,567 jobs 10. Renewable energy dominates these approvals, with 179 projects valued at PHP 5.21 trillion9. Perhaps most significantly, the BOI is currently assessing 10 additional strategic projects exceeding PHP 1 trillion, including four offshore wind projects with combined 3.7 GW capacity 11.

World Bank Charts the Course for Philippine Offshore Wind

Technical potential assessment of 178 GW

The Department of Energy and World Bank Group launched the Offshore Wind Roadmap for the Philippines in April 2022, establishing a strategic framework for offshore wind Philippines development 212. The assessment identified 178 GW of technical offshore wind potential within 200 kilometres of the shoreline 23. This evaluation utilised wind resource data from the Global Wind Atlas version 3.0, which provides information at 250-metre resolution based on contemporary modelling methodologies 13.

What strikes me about this roadmap is how it moves beyond simple resource assessment to create a genuine strategic framework. Unlike many development studies that gather dust on shelves, this one appears designed to actually guide policy decisions.

Tale of two futures: growth scenarios that matter

The roadmap presents two starkly different development pathways, and frankly, the contrast is quite sobering. The low growth scenario projects 3 GW of installed capacity by 2040, supplying 3.3% of the country's electricity demand314. The high growth alternative forecasts 21 GW of capacity, meeting 21% of electricity requirements by the same timeframe1415. Both scenarios examine technical, economic, environmental, social, employment, and financing dimensions of establishing the offshore wind farm Philippines market2.

The difference between these scenarios isn't just academic – it represents fundamentally different economic futures for the Philippines.

Economic stakes that demand attention

The high growth scenario delivers substantially greater economic benefits, and the numbers are quite remarkable. Local gross value added reaches £11.44 billion by 2040, compared to £0.87 billion under low growth projections15. Employment figures similarly diverge, with the high scenario generating 205,000 jobs against 15,000 in the low scenario15. The larger market scale drives 32% lower levelised cost of energy by 2040 through increased local capabilities and accelerated risk reduction15.

These aren't just statistics on a spreadsheet – they represent the difference between creating a genuine offshore wind manufacturing ecosystem and remaining dependent on imported technology and expertise.

Deep water advantage: floating technology dominance

Perhaps the most intriguing aspect of the Philippines' offshore wind potential lies beneath the waves. Essentially, 90% of the technical potential suits floating offshore wind installations8. The assessment identifies 160 GW suitable for floating turbine generators in waters deeper than 60 metres, whilst 18 GW applies to fixed-bottom foundations313. This distribution reflects the archipelago's bathymetric characteristics, where substantial offshore wind Philippines resources exist in deep water areas requiring floating technology solutions.

This deep-water dominance actually positions the Philippines rather well for the future of offshore wind. Floating technology represents the next frontier of the industry, and countries that master it early could find themselves at a significant advantage.

Building the Backbone – Infrastructure and Grid Strategy

Competitive Renewable Energy Zones framework

The government's approach to infrastructure development centres on the Competitive Renewable Energy Zones programme, essentially creating designated areas where renewable energy potential and developer interest converge 1617. It's quite a sensible approach really – the DOE designed this framework to tackle the usual suspects that plague renewable projects: transmission access bottlenecks, energy curtailment issues, and the inevitable regulatory hurdles 16. Whilst offshore wind projects aren't required to locate within these CREZs, there's a clear advantage in doing so when it comes to grid connection.

National Grid transmission development plan

The National Grid Corporation of the Philippines has initiated consultations for its Transmission Development Plan covering 2025 to 2050, and it's becoming clear that earlier estimates significantly underestimated offshore wind potential 18. The TDP acknowledges this reality, recognising that substantial transmission backbone development will be necessary16. The proposed modifications are quite ambitious: 500kV backbone extensions on both western and eastern sides of northern Luzon, strategically positioning new 500kV substations closer to offshore wind locations rather than forcing connections through the existing Laoag 230 Substation, and implementing a 500kV backbone within Mindoro island16[141].

Two specific projects stand out in the 2031-2040 timeline: the Alas-Asin 500kV Substation will accommodate offshore wind plants at Manila Bay and offshore Mariveles, whilst the Calatagan 500kV Substation will serve projects at Calatagan Bay and offshore Northern Mindoro16[141]. These aren't just technical upgrades – they represent the foundational infrastructure that will determine whether the Philippines can actually deliver on its offshore wind ambitions.

Port modernisation initiatives

The Asian Development Bank's engagement with NIRAS to conduct pre-feasibility studies for expanding ten ports as offshore wind facilities shows just how serious the infrastructure planning has become 19. Three ports have received priority attention, and the numbers are quite telling: Currimao in Ilocos Norte (supporting 9,489 MW across 13 service contracts), Batangas in Santa Clara with an impressive 24,300 MW across 29 contracts, and Jose Panganiban in Camarines Norte handling 8,150 MW across 14 contracts 20. These aren't just port upgrades – they're the manufacturing and logistics hubs that will make or break the sector's development.

South Luzon offshore wind grid connectivity

The Batangas-Mindoro Interconnection Project exemplifies the scale of grid infrastructure required, linking Mindoro to the Luzon Grid through a 28.5km submarine cable designed at 500kV voltage16[141]. The timeline is quite aggressive: Stage 1 reaches completion in September 2027, with Stage 2 finished by December 2030 16. Already, grid connection agreements have secured 1.65 GW capacity across three projects: Frontera Bay (450 MW), Guimaras Strait (600 MW), and Guimaras Strait II (600 MW)2122. It's a clear signal that developers are moving beyond planning phases into serious commitment territory.

The Auction That Could Change Everything

GEA-5: Philippines Takes the Plunge

March 2026 marked a watershed moment when the Department of Energy opened registration for GEA-5 on 2 March, closing just two weeks later on 16 March 23. The Energy Regulatory Commission set a ceiling price of PHP 11.00 per kilowatt-hour24, which frankly represents an ambitious benchmark for what remains an untested market. The auction proper occurs on 27 August 2026, with winning bidders announced by 22 September 2324.

This marks the Philippines' first auction dedicated exclusively to fixed-bottom offshore wind, offering 3,300 MW capacity for delivery between 2028 and 2033. The format operates on a pay-as-bid basis, with bids ranked on price subject to technical and eligibility requirements 16. It's a bold move for a country that has never built a single offshore wind turbine.

Service Contracts Tell a Different Story

The numbers behind the scenes are rather more impressive than the modest GEA-5 offering might suggest. The DOE has awarded 92 Offshore Wind Energy Service Contracts representing 66 GW of potential capacity3. That's roughly equivalent to the entire installed electricity capacity of the United Kingdom, which puts the scale into perspective.

Notable contracts include BlueFloat Energy's four floating offshore wind sites totalling 7.5 GW3, and BuhaWind Energy Philippines' 2 GW project offshore Ilocos Norte, scheduled for full operation by 2030 3. These figures demonstrate that whilst GEA-5 might be cautious, developer appetite certainly isn't.

Copenhagen Infrastructure Partners Leads the Charge

Copenhagen Infrastructure Partners secured three service contracts in 2023 for 2 GW capacity across Camarines Norte, Camarines Sur, Northern Samar, Pangasinan, and La Union 25. The flagship San Miguel Bay project carries a 1 GW capacity with USD 3 billion investment 26. CIP sold a 25% stake to ACEN in May 2025 26, which suggests confidence in the market's commercial viability.

CIP's involvement is particularly significant because they bring proven expertise from European offshore wind markets. Their participation validates the Philippines as a serious offshore wind destination, not merely an experimental market.

The Bankability Question

Here's where things get interesting (and challenging). Winning bidders receive the Green Energy Tariff through 20-year Renewable Energy Payment Agreements with TransCo 16. However, early project tariffs could range from PHP 9.1 to PHP 16.4 per kWh, requiring concessional financing from multilateral development banks and export credit agencies to achieve bankability 27.

The gap between the GEA-5 ceiling price and these projected costs highlights the sector's fundamental challenge. Without development bank support, many projects simply won't stack up financially. This isn't unusual for emerging offshore wind markets, but it does mean the government needs to be realistic about the pace of development.

Conclusion

The offshore wind farm Philippines sector stands at a transformative juncture, supported by comprehensive policy reforms, strategic infrastructure planning, and substantial technical potential. With 178 GW identified and 66 GW already under service contracts, the inaugural GEA-5 auction represents a crucial market test. Bankability remains the sector's primary challenge, requiring concessional financing to bridge early-stage cost gaps. Success in these foundational projects will unquestionably determine whether the Philippines achieves its ambitious renewable energy targets by 2040.

FAQs

Q1. What is the technical potential for offshore wind energy in the Philippines?

The Philippines has a technical offshore wind potential of 178 GW within 200 kilometres of the shoreline. Of this capacity, approximately 160 GW is suitable for floating turbine installations in waters deeper than 60 metres, whilst 18 GW can accommodate fixed-bottom foundations.

Q2. What are the Philippines' renewable energy targets for 2030 and 2040?

The National Renewable Energy Programme aims to achieve a 35% renewable energy share in power generation by 2030 and increase this to 50% by 2040. Meeting these targets requires adding 52.8 GW of new renewable capacity, including 16.7 GW from wind energy.

Q3. Can foreign companies fully own offshore wind projects in the Philippines?

Yes, foreign investors can now hold 100% equity in Philippine entities engaged in renewable energy projects. The Department of Energy removed the previous 60% Filipino ownership requirement in November 2022, allowing international companies full operational and profit control.

Q4. What is the Fifth Green Energy Auction (GEA-5) for offshore wind?

GEA-5 is the Philippines' first auction dedicated exclusively to fixed-bottom offshore wind, offering 3,300 MW capacity for delivery between 2028 and 2030. The auction operates on a pay-as-bid basis with a ceiling price of PHP 11.00 per kilowatt-hour, and winning bidders receive 20-year Renewable Energy Payment Agreements.

Q5. How many offshore wind service contracts have been awarded in the Philippines?

The Department of Energy has awarded 92 Offshore Wind Energy Service Contracts representing 66 GW of potential capacity. Notable projects include BlueFloat Energy's 7.5 GW across four sites and Copenhagen Infrastructure Partners' 2 GW capacity across multiple provinces.