Offshore Wind Project Staffing: EU vs APAC - The Reality of Scaling Site Teams

Offshore Wind Project Staffing: EU vs APAC - The Reality of Scaling Site Teams

APAC's ambitious target of 295 GW by 2034 arrives at a time when the global wind sector already faces a projected 6-8% shortage of qualified technicians by 2028. Each gigawatt demands hundreds of skilled professionals, yet the challenge extends far beyond simple recruitment arithmetic. Europe operates with established talent pools but faces fierce competition for experienced site leaders. APAC presents rapid capacity growth against uneven workforce planning depth, where Taiwan's 3.04 GW of commercial operations sits alongside markets still grappling with grid readiness and local content requirements.

The timing pressures that destroy offshore wind projects often stem from workforce planning that starts too late in the development cycle. Reactive hiring creates a cascade of problems: rushed decisions, top talent lost to competitors within 10 days, and site roles treated with equal urgency regardless of project sequencing. Commissioning managers and HV specialists cannot mobilize until predecessor activities complete, yet many projects hire these roles in parallel with foundation teams.

Europe's paradox illustrates the complexity clearly. Despite projections of 607,000 jobs by 2030, urgent shortages persist for 7,000 blade technicians and 6,500 field engineers. Talent density exists, but role scarcity intensifies competition rather than solving availability problems. APAC markets present the opposite challenge: fast growth across countries at dramatically different maturity levels, requiring strategies that account for varying regulatory frameworks and contractor ecosystems.

The solution lies in anticipating workforce needs months before mobilization rather than reacting to vacancies as they appear. Phased hiring plans aligned to construction stages, combined with regional market mapping and blended permanent-freelance strategies, create the foundation for successful project delivery. This article examines the real hiring and mobilization realities facing project directors and construction leaders across both regions, exploring contractor ecosystems, timing pressures, and the strategic workforce planning that separates successful projects from those derailed by staffing delays.

The Hidden Complexity Behind Those Workforce Numbers

Scaling site teams for offshore wind feels deceptively straightforward until you examine what sits beneath those capacity targets. Workforce constraints operate through structural problems that recruitment budgets cannot solve quickly, regardless of size. Four levels of constraint define this challenge: market fragmentation, project phasing realities, mobility barriers, and the timing misalignment between project awards and workforce readiness.

Competing for Talent Across Five Industries

Offshore wind recruitment does not occur in isolation. Projects compete for skilled professionals across oil and gas, shipbuilding, marine operations, power transmission, and construction. Around 90% of oil and gas competencies transfer to offshore wind, meaning recruitment draws from overlapping sectors rather than a dedicated wind talent pool. Each sector follows its own demand cycles. Companies chase the same experienced contractors, slowing mobilization and driving costs higher.

The contractor ecosystem adds another layer of complexity. Projects operate through fragmented tiers involving special project vehicles, tier 1 contractors such as Siemens Gamesa, tier 2 sub-contractors handling civil engineering or components, and tier 3 specialists. This structure deepens when workers operate as self-employed consultants—one estimate suggests 57% of the construction services workforce falls into this category. Multiple contracting layers make it harder to compare pay, inhibit collective negotiation, and reduce redeployment opportunities when projects conclude.

Project Phases Demand Different Workforce Configurations

Site teams expand and contract through distinct project phases rather than maintaining static headcounts. Construction creates surge demand for hundreds of roles through 2026, then operations roles increase post-2028. Regional demand patterns differ significantly. The UK's 39GW baseline scenario shows offshore wind workforce demand peaking above 74,000 in 2030, climbing to nearly 95,000 under the 52GW scenario. Europe faces shortages of 7,000 blade technicians, 6,500 field engineers, and 5,000 pre-assembly technicians before 2030. Global technician requirements climb from 475,000 in 2025 to 628,000 by 2030—a 50% increase over five years.

Project teams often discover that certain roles cannot be hired simultaneously. Commissioning managers, HV specialists, and site leadership require predecessor activities to complete before mobilization becomes possible. Treating all site roles as equally urgent creates inefficient hiring patterns.

Cross-Border Mobility Remains Constrained

Geographic proximity does not guarantee workforce mobility, even within Europe. Regulatory complexity across countries, varied labor laws, and language differences prevent seamless talent movement. Certification requirements differ by jurisdiction. Project timelines leave minimal room for error, and non-compliance triggers costly delays or penalties.

Training capacity represents a frequently overlooked element in workforce planning. Scaling the wind workforce requires up to ten years, whether through training sufficient technician volumes or improving retention rates. Many UK trainees remain unable to secure employment in the wind sector due to limited opportunities, risking certification expiry and wasting government investment. Training lead times require earlier visibility of the project pipeline so investors and training providers can commit to local skills development.

Project Awards Arrive Too Late for Strategic Planning

Contract awards occur too late in the development cycle for effective workforce planning. CfD awards become available very late in the development process, after consent is already in place. For highly skilled roles, CfD awards can occur too late to enable investment in developing local labor. Employers face managing labor shortages and under-skilled candidates during critical project periods.

Pipeline uncertainty compounds these timing problems. Primary reasons for reducing or freezing recruitment include project pipeline reductions, investment uncertainty, and cost pressures. Without a stable framework supporting energy system components, the sector risks losing experienced professionals and deterring new entrants. Business certainty proves essential to scaling a skilled workforce and avoiding boom-and-bust cycles. This becomes achievable only through consistent, visible project pipelines.

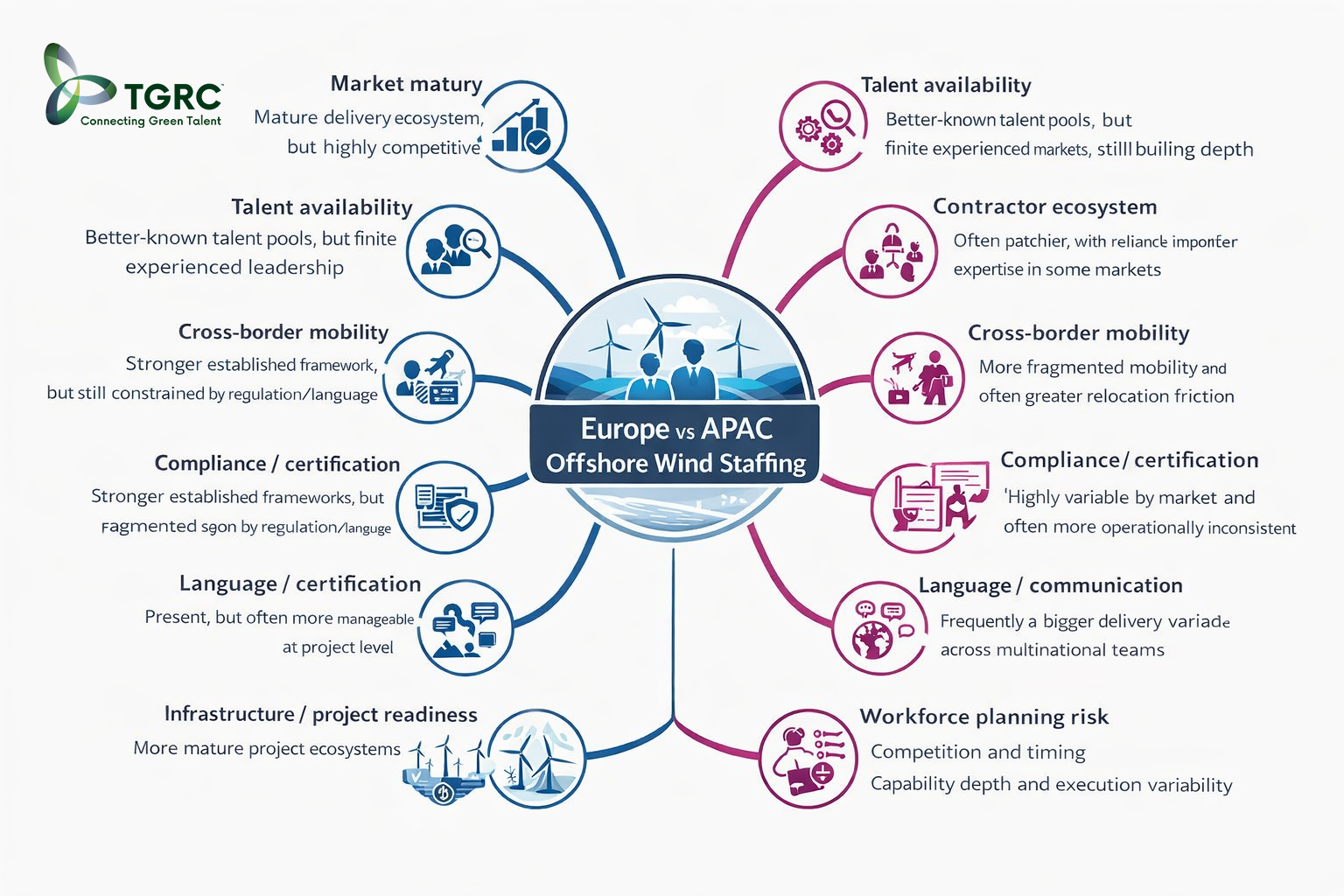

Europe's Paradox: When Experience Creates Competition, Not Solutions

Europe's offshore wind sector presents a fascinating contradiction. After decades building the world's most mature wind industry, the continent now faces its most acute staffing challenges. The region operates with established training pathways, deep contractor networks, and project delivery experience that spans back to Denmark's first offshore installations in the 1990s. Yet this very maturity creates intense competition for experienced professionals rather than solving availability problems.

Europe's wind energy workforce is set to grow from 443,000 jobs to 607,000 by 2030, with offshore wind accounting for 20% of direct roles. Manufacturing represents nearly half of direct employment, supported by more than 250 factories. This concentration suggests talent pools exist, but accessing them remains surprisingly constrained.

The Numbers Game: Talent Density Meets Role Scarcity

Workforce growth projections mask critical gaps in specific competencies. Europe faces urgent demand for 7,000 blade technicians, 6,500 field engineers, and 5,000 pre-assembly technicians before 2030. Eight out of ten critical roles experiencing the largest shortages rely on vocational education and training. The sector currently supports 211,000 direct roles across development, manufacturing, installation, operation, and decommissioning.

What's particularly telling is how role scarcity intensifies as projects mature. Operations and maintenance functions require higher skill density than early construction phases. This increases competition for experienced technical profiles capable of working with complex mechanical systems, hydraulics, electrical installations, and fault diagnostics in exposed marine environments.

Policymakers recognize the challenge. Scaling up training programs for key roles, encouraging retraining workers from other sectors, harmonizing certifications, and enabling EU-wide skills mobility have all become policy priorities. However, implementation remains uneven across member states.

The Maritime Migration: High Mobility, Limited Availability

Offshore wind recruitment draws heavily from the maritime labor market, with the strongest pressure appearing where skills transfer easily and offshore operational experience is already well established. Marine operations personnel, experienced officers, and deck crews from offshore support vessels increasingly move into wind farm construction and operations activities.

For many seafarers and offshore professionals, this career transition proves attractive. Maritime employers report higher turnover in experienced mid-career profiles, particularly among officers, DP operators, and technical staff. WindEurope highlights retention as a growing concern as demand accelerates faster than workforce inflow.

The financial dynamics are straightforward. Offshore wind recruitment drives up day rates and salary expectations in overlapping role categories, forcing vessel operators to either absorb higher crewing costs or adjust commercial terms. The same experienced professionals find themselves with multiple competing offers, often with minimal notice periods.

Borders That Still Matter

Legal and regulatory barriers continue to hinder development of cross-border offshore wind projects. Member states operate under different legal systems, and this fragmentation complicates joint planning and infrastructure development. Critics argue that current frameworks lack the efficiency and legal force needed to support complex transboundary projects.

Offshore wind projects frequently span multiple jurisdictions, especially in the North Sea and Baltic regions. Crewing models now integrate visa management, medical validity tracking, and local labor compliance earlier in the recruitment process. Regulatory fragmentation increases the administrative load on employers and recruiters alike.

The CV Carousel: When Everyone Knows Everyone

Perhaps the most revealing aspect of Europe's mature market is how recruitment increasingly favors candidates with prior maritime compliance experience, as workforce readiness in this area directly affects project scalability. The emphasis moves from job titles to deployable competence, availability, and compliance readiness.

Agencies with offshore wind-specific knowledge, training partnerships, and regional compliance expertise are better positioned to support complex projects. Over time, this creates a clearer separation between agencies that focus on volume recruitment and those that operate as long-term workforce partners for offshore wind and maritime clients.

The result is a market where the same CVs circulate repeatedly among the same recruiters and hiring managers. Experience becomes the primary differentiator, but experienced professionals remain a finite resource.

APAC: Where Rapid Growth Meets Reality

APAC offshore wind markets present a fascinating paradox: explosive capacity targets alongside workforce planning that ranges from sophisticated to virtually non-existent, depending on which border you cross. Taiwan operates 3.04 GW commercially and ranks seventh globally. China dominates with 42.7 GW installed—the world's largest offshore wind market—backed by annual turbine manufacturing capacity exceeding 20 GW. Yet beyond these established players, the picture becomes more complex. Japan targets 5.7 GW, South Korea 14.3 GW, Vietnam 6.0 GW, and Taiwan 10.9 GW by 2030. Industry forecasts suggest Taiwan will hit 91% of its target and Japan over 70%, while South Korea and Vietnam may struggle to reach even 50%.

The Maturity Spectrum Creates Different Workforce Challenges

Taiwan, despite ongoing challenges, has successfully established commercial-scale projects with international developers including Ørsted, Corio Generation, TotalEnergies, and EDF actively operating. The pipeline shows almost 48 GW of potential capacity with 2.2 GW currently under construction. South Korea reached a milestone in 2024 when the 99 MW Jeonnam 1 project achieved commercial operation after securing financial close in 2023. Japan passed legislation enabling offshore wind development in its Exclusive Economic Zone, addressing the practical constraints of deep coastal waters and limited nearshore space. Australia maintains a structured approach with feasibility licenses awarded to six Gippsland zone projects. The Philippines has scheduled its first offshore wind auction for 2026, targeting 3,300 MW.

Each market stage demands different workforce strategies. Taiwan's experience shows how established markets still face contractor bottlenecks. Emerging markets like the Philippines struggle with basic infrastructure readiness.

Local Content Policies Meet Practical Workforce Constraints

Taiwan's journey with local content mandates illustrates the tension between policy ambitions and delivery reality. The country eventually committed to greater flexibility in Round 3.2 projects and agreed to drop localization requirements from future allocation rounds, whether as eligibility conditions or award criteria. The practical consequences became clear in May when Taiwan's Ministry of Economic Affairs revoked development rights for Corio's Haiding 1 and Enervest's Deshuai wind farms under Phase 3-2, representing 600 MW of combined capacity, after both projects failed reviews. Vietnam's policy direction favors local developers, demonstrated when German developer PNE lost a major project to a newly created subsidiary of domestic conglomerate Vingroup despite nearly six years of preparation.

These policy shifts create workforce planning uncertainty. International contractors cannot commit to training local workers without project certainty, yet local content requirements demand this investment.

Infrastructure Bottlenecks That Workforce Cannot Solve

Foundation installation vessels represent perhaps the most critical constraint. About a dozen vessels capable of handling 2,000-ton+ monopoles operated at full utilization in 2024. Industry forecasts between 2030-2035 suggest pent-up demand will require an additional 15 FIVs equipped with larger cranes. Philippine ports were never designed for offshore wind logistics and require costly upgrades before projects can proceed. Grid readiness remains questionable even where projects advance, with transmission planning consistently lagging behind generation development.

Workforce scaling becomes secondary when basic infrastructure cannot support project delivery.

Communication Complexity Europeans Never Face

Multinational site teams operating across APAC markets encounter communication barriers that European projects rarely experience at comparable scale. Projects involving European turbine technology, Korean vessels, and local workforce coordination require language protocols embedded into safety procedures and commissioning workflows from day one. This adds layers of complexity to recruitment that European projects, operating within more linguistically homogeneous regions, simply do not face.

The practical impact extends beyond translation. Technical specifications, safety protocols, and quality procedures must work across language barriers under time pressure and offshore conditions.

Five Mistakes That Sink Offshore Wind Hiring Before Projects Even Start

Project teams lose the talent war not because skilled professionals are unavailable, but because recruitment strategies create their own problems. The same five mistakes surface repeatedly, whether you're building in the North Sea or the South China Sea.

Waiting Until the Phone Rings

Here's a reality check: offshore wind projects need at least six months to fill critical vacancies, yet most hiring starts only when someone quits or a milestone looms. German energy technician roles average six months from posting to placement. React to gaps rather than anticipate them, and you're left with rushed decisions and panic hiring.

The mathematics work against delay. Top candidates move to new roles within 10 days of serious interest. Slow approval processes and scheduling delays hand talent directly to competitors who move faster.

The Skills Transfer Myth

Oil and gas professionals share roughly 60% skills overlap with floating offshore wind, but transitions aren't automatic. Salary expectations from traditional energy sectors often clash with renewable energy budgets. Cultural gaps exist between cost-reduction innovation models and established engineering approaches.

The competence barrier hits hardest with wind-specific experience requirements. Expecting candidates to check every technical box in specialized areas unnecessarily shrinks talent pools. Better to hire for core competencies and train for wind specifics.

Fishing in the Same Pond

Renewables companies compete primarily within their own sector rather than developing internal talent or recruiting from adjacent industries. Hiring managers default to poaching from other green energy firms instead of building capacity.

This creates a circular problem. Some 77% of renewables professionals would consider leaving for other industries within three years, with technology being the most attractive alternative. The sector keeps fighting over the same people rather than expanding the talent base.

The Parallel Hiring Trap

Not all site roles can start simultaneously. Commissioning managers and HV specialists need predecessor activities completed before they can mobilize effectively. Hiring everyone in parallel wastes recruiter bandwidth and creates coordination headaches.

Project phases demand different workforce configurations. Understanding these sequences prevents inefficient resource allocation.

Process-Free Speed Hiring

Compressed timelines and shifting start dates frustrate candidates and recruiters alike. Poor coordination between project leads, HR, and recruitment teams delays essential decisions. Without clear workflows, contractors lose patience and projects lose access to available talent.

Speed without process generates bad hires. Clear hiring workflows, even under pressure, produce better outcomes than chaotic scrambles.

Building Site Teams That Actually Deliver

The best workforce planning starts before you need it. Like Henry Ford's approach to manufacturing, offshore wind projects succeed when they anticipate demand rather than react to it. Effective project staffing means thinking months ahead of mobilization, not scrambling when vacancies appear.

Match Your Hiring to How Projects Actually Unfold

Different project phases demand entirely different workforce configurations. The team that secures planning consent bears little resemblance to the crew installing turbines 18 months later. Smart project leaders map their hiring requirements to each phase of development, positioning candidates well before contract awards hit the desk.

This sequencing matters more than most realize. Commissioning managers and HV specialists cannot start until predecessor activities complete. Hiring them alongside foundation crews wastes time and money.

Know Your Regional Talent Landscape Before the Rush

Pre-established candidate pipelines separate successful projects from delayed ones. When project acceleration hits, starting recruitment from scratch guarantees you'll lose the best people to competitors who planned ahead. Regional recruitment partners with offshore wind presence anticipate these workforce requirements, reducing the gap between contract signature and boots on deck.

The difference between having a talent map and not having one can determine whether your project launches on schedule or joins the statistics of delayed offshore wind developments.

Blend Your Workforce Strategy With Project Reality

Annual headcount planning works for office jobs, not offshore wind projects. Delivery milestones drive workforce demand, not calendar years. The most effective projects use blended models combining permanent staff, contractors, and project-based specialists aligned to delivery peaks.

Identifying scarce roles early and building talent pools before peak competition begins strengthens your execution capability when it matters most. This approach proves particularly valuable for roles where certification and compliance requirements can take months to arrange.

Partner With Recruiters Who Understand Wind Projects

Sector-specialist recruiters maintain relationships with in-demand professionals, including those not actively seeking new roles, and grasp technical requirements across entire project lifecycles. They stay current with compliance requirements for deploying workers across specific markets, reducing legal risk that can derail timelines. For multi-phase programs, faster and more accurate placements translate directly into reduced project risk.

Generic recruitment approaches fail in offshore wind because the technical requirements, safety standards, and project phasing create unique hiring challenges that require specialized knowledge.

Succession Planning Prevents Knowledge Drain

Structured succession planning ensures no single person becomes a project bottleneck. Strong succession frameworks preserve technical knowledge, reduce operational downtime, and strengthen retention strategies for always-in-demand capabilities including controls, electrical, and commissioning roles. Without these plans, decades of tacit knowledge walk away with retirement or job changes.

The offshore wind sector cannot afford to lose institutional knowledge when projects depend on understanding complex technical systems and regulatory environments that take years to master.

Conclusion

Offshore wind project staffing cannot be reduced to a simple EU versus APAC comparison. Europe operates with mature talent pools but faces intense competition for experienced site leadership. APAC presents rapid capacity growth against uneven workforce planning depth and varying regulatory frameworks country by country.

In truth, both regions face the same core challenge: securing the right people, in the right place, at the right stage of the project, fast enough to prevent delivery risk. Workforce planning must start months before mobilization, not when vacancies appear.

For organizations scaling wind delivery teams across multiple markets, TGRC supports with market mapping, talent intelligence, and targeted hiring that accounts for regional execution realities.

FAQs

Q1. What makes offshore wind project staffing so challenging in 2026?

Offshore wind projects face a projected 6-8% global shortage of qualified technicians by 2028, with demand for hundreds of skilled professionals per gigawatt of capacity. The challenge isn't just finding people—it's securing the right specialists at the right project phase, fast enough to avoid delays. Competition spans multiple industries including oil and gas, shipbuilding, and marine sectors, all competing for the same talent pool.

Q2. How do offshore wind workforce needs differ between Europe and APAC?

Europe operates with mature talent pools but faces intense competition for experienced professionals, particularly for roles like blade technicians, field engineers, and pre-assembly specialists. APAC presents rapid capacity growth with uneven workforce depth—markets like Taiwan and China have established ecosystems, while countries like Vietnam and the Philippines are still developing their contractor networks and regulatory frameworks.

Q3. What are the most common hiring mistakes in offshore wind projects?

Projects typically start recruitment too late, often only six months before mobilization when roles can take that long to fill. Other critical mistakes include assuming skills transfer cleanly across markets without accounting for cultural differences, over-relying on a narrow talent pool within renewables, treating all site roles as equally urgent, and rushing hiring decisions without proper processes.

Q4. Why can't offshore wind projects simply recruit more people to solve staffing shortages?

The labor market is fragmented across multiple competing sectors, with around 90% of oil and gas competencies transferring to offshore wind. Training new technicians takes up to ten years, and regulatory complexity across borders limits mobility. Additionally, site teams are dynamic—construction phases require different workforce configurations than operations, making it impossible to simply scale headcount uniformly.

Q5. What does effective workforce planning look like for offshore wind projects?

Successful planning involves phased hiring aligned to construction stages, regional market mapping before needs arise, and blended strategies using permanent and freelance workers. Projects should begin workforce planning months before mobilization, build candidate pipelines early with specialist recruiters, and implement succession planning for site leadership to prevent knowledge loss and maintain continuity.